All Categories

Featured

Table of Contents

- – What are the benefits of using Financial Indep...

- – Can I use Infinite Banking for my business fin...

- – How do I optimize my cash flow with Cash Flow...

- – Bank On Yourself

- – What is the minimum commitment for Infinite ...

- – Wealth Building With Infinite Banking

- – What are the most successful uses of Infinit...

Term life is the ideal remedy to a short-term need for safeguarding versus the loss of an income producer. There are far fewer factors for irreversible life insurance policy. Key-man insurance and as component of a buy-sell agreement entered your mind as a possible good factor to purchase a permanent life insurance policy plan.

It is an expensive term created to offer high valued life insurance with adequate commissions to the agent and substantial earnings to the insurance provider. Self-financing with life insurance. You can reach the very same end result as infinite banking with better outcomes, more liquidity, no risk of a policy gap setting off a massive tax issue and more options if you utilize my options

What are the benefits of using Financial Independence Through Infinite Banking for personal financing?

My bias is good details so come back below and read even more articles. Compare that to the predispositions the marketers of infinity banking get. Here is the video from the promoter utilized in this article. 5 Blunders Individuals Make With Infinite Banking.

As you approach your golden years, monetary protection is a leading concern. Among the several various monetary approaches available, you may be hearing an increasing number of regarding infinite banking. Bank on yourself. This principle allows almost any individual to become their very own bankers, using some advantages and flexibility that can fit well into your retirement

Can I use Infinite Banking for my business finances?

The funding will certainly accrue easy interest, yet you preserve versatility in establishing settlement terms. The rates of interest is also typically lower than what you would certainly pay a typical bank. This kind of withdrawal allows you to access a portion of your money value (up to the amount you've paid in costs) tax-free.

Lots of pre-retirees have worries about the safety of limitless banking, and for great reason. The returns on the cash money value of the insurance plans might fluctuate depending on what the market is doing.

How do I optimize my cash flow with Cash Flow Banking?

Infinite Financial is a financial method that has actually gained considerable interest over the previous couple of years. It's a special technique to handling personal finances, enabling individuals to take control of their cash and produce a self-reliant financial system - Financial leverage with Infinite Banking. Infinite Banking, likewise recognized as the Infinite Banking Idea (IBC) or the Count on Yourself technique, is a financial method that entails using dividend-paying entire life insurance policy policies to develop a personal banking system

To understand the Infinite Banking. Concept technique, it is therefore important to give an introduction on life insurance as it is an extremely misunderstood asset class. Life insurance policy is a vital component of economic planning that provides several benefits. It comes in several sizes and shapes, one of the most typical kinds being term life, whole life, and universal life insurance policy.

Bank On Yourself

Allow's explore what each type is and exactly how they vary. Term life insurance policy, as its name recommends, covers a details period or term, usually in between 10 to 30 years. It is the simplest and usually one of the most inexpensive sort of life insurance. If the policyholder passes away within the term, the insurer will pay the fatality benefit to the assigned beneficiaries.

Some term life plans can be restored or transformed into an irreversible policy at the end of the term, yet the premiums usually enhance upon revival as a result of age. Whole life insurance policy is a sort of irreversible life insurance policy that supplies insurance coverage for the policyholder's whole life. Unlike term life insurance policy, it includes a cash money value element that grows with time on a tax-deferred basis.

It's vital to keep in mind that any impressive finances taken versus the policy will certainly decrease the fatality advantage. Whole life insurance coverage is commonly extra costly than term insurance due to the fact that it lasts a life time and constructs money value. It also supplies predictable premiums, meaning the price will certainly not raise gradually, providing a degree of certainty for insurance holders.

What is the minimum commitment for Infinite Banking In Life Insurance?

Some reasons for the misconceptions are: Complexity: Whole life insurance policies have more intricate attributes contrasted to describe life insurance policy, such as cash money worth accumulation, rewards, and policy lendings. These attributes can be testing to comprehend for those without a history in insurance or individual finance, bring about complication and false impressions.

Predisposition and misinformation: Some people might have had adverse experiences with entire life insurance coverage or listened to tales from others that have. These experiences and anecdotal information can contribute to a prejudiced view of whole life insurance policy and perpetuate misunderstandings. The Infinite Financial Concept approach can only be executed and performed with a dividend-paying whole life insurance coverage policy with a shared insurance provider.

Whole life insurance policy is a sort of long-term life insurance policy that offers coverage for the insured's entire life as long as the premiums are paid. Entire life policies have two major components: a death advantage and a cash value (Financial independence through Infinite Banking). The survivor benefit is the amount paid out to recipients upon the insured's death, while the cash money value is a financial savings component that expands with time

Wealth Building With Infinite Banking

Dividend repayments: Common insurance provider are possessed by their insurance policy holders, and consequently, they might distribute profits to policyholders in the type of dividends. While returns are not assured, they can help enhance the cash worth growth of your policy, raising the overall return on your capital. Tax advantages: The money worth development within an entire life insurance policy plan is tax-deferred, meaning you don't pay tax obligations on the growth up until you take out the funds.

This can offer substantial tax obligation advantages compared to other savings and financial investments. Liquidity: The cash value of a whole life insurance policy plan is highly liquid, allowing you to accessibility funds easily when needed. This can be particularly important in emergencies or unforeseen financial situations. Asset protection: In numerous states, the cash worth of a life insurance plan is shielded from lenders and suits.

What are the most successful uses of Infinite Banking Wealth Strategy?

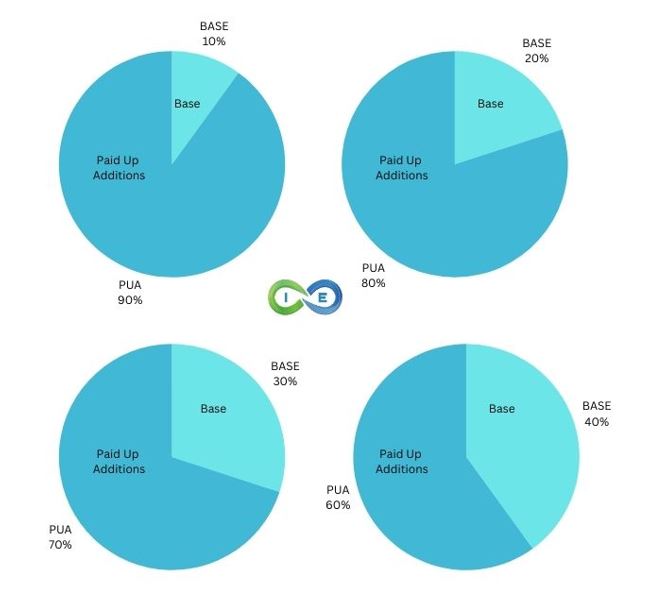

The policy will certainly have instant cash value that can be positioned as security 30 days after moneying the life insurance policy plan for a rotating line of credit score. You will certainly have the ability to access via the revolving credit line up to 95% of the offered cash worth and utilize the liquidity to fund an investment that gives earnings (cash money circulation), tax obligation benefits, the possibility for gratitude and leverage of other individuals's ability, capabilities, networks, and funding.

Infinite Banking has actually come to be really prominent in the insurance policy world - also much more so over the last 5 years. R. Nelson Nash was the maker of Infinite Financial and the organization he founded, The Nelson Nash Institute, is the only organization that officially accredits insurance coverage representatives as "," based on the following criteria: They straighten with the NNI requirements of professionalism and trust and ethics (Tax-free income with Infinite Banking).

They effectively finish an apprenticeship with an elderly Authorized IBC Professional to guarantee their understanding and capacity to apply all of the above. StackedLife is Authorized IBC in the San Francisco Bay Location and works nation-wide, helping customers recognize and implement The IBC.

{kind=link}

Table of Contents

- – What are the benefits of using Financial Indep...

- – Can I use Infinite Banking for my business fin...

- – How do I optimize my cash flow with Cash Flow...

- – Bank On Yourself

- – What is the minimum commitment for Infinite ...

- – Wealth Building With Infinite Banking

- – What are the most successful uses of Infinit...

Latest Posts

Whole Life Insurance-be Your Own Bank : R/personalfinance

Ibc Private Bank

Ibc Concept

More

Latest Posts

Whole Life Insurance-be Your Own Bank : R/personalfinance

Ibc Private Bank

Ibc Concept